The Two Variances in Direct Materials Cost Are

There are two components to material variances. The standard direct labor rate.

Compute And Evaluate Materials Variances Principles Of Accounting Volume 2 Managerial Accounting

Standard Quantity for Actual Output x.

. The direct materials price variance is caused by paying too much or too little for material. Materials quantity variance AQU SQ SP. Direct materials quantity d.

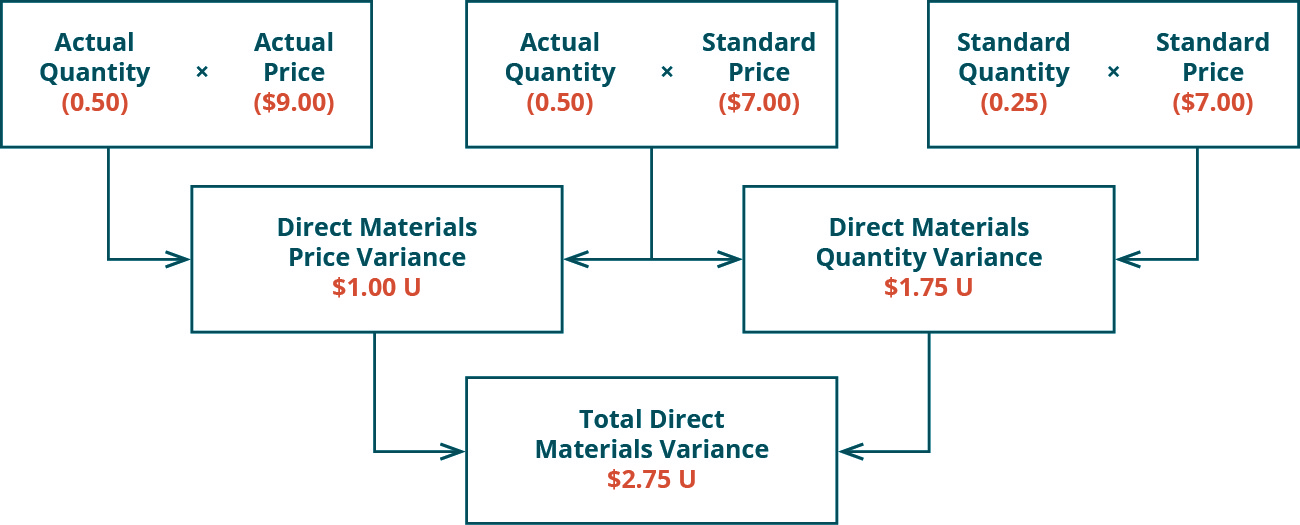

Change increase decrease in the quantity of materials used. Actual Quantity 050 times Actual Price 900 and Actual Quantity 050 times Standard Price 700 combine to point to Second row box. This difference comes to a 13500 favorable variance meaning that the company saves 13500 by buying direct materials for 990 rather than the original standard price of 1035.

Ft 1300 hr Standard Cost SC 110 sq. Direct labor time b. The following material variances are calculated.

A PDOH rate activity-based costing scheme equivalent units etc. 4000 hours were worked at the cost of 36000. Among cost variances I find overhead variances to be less useful than direct labor or direct materials variances.

Direct Material Price Variance 100 U. The direct materials price variance and the direct materials quantity variance. Cost Variance Actual Cost x Actual Quantity Standard Cost x Actual Quantity Actual Cost Standard Cost x Actual Quantity AC-SC x AQ Direct Direct Materials Labor Actual Cost AC 105 sq.

Direct materials 19000 Direct labor 14630 Total 33630 The standard materials price is 050 per pound. Change increase decrease in the price of materials. The direct labor quantity standard is usually referred to as labor efficiency variance while the price.

None of these choices are correct. Standard Mix of Actual Quantity x Standard Price. Material Cost variance.

The direct material price variance is the difference between standard cost and the actual cost for the actual quantity of material used for production. The purchasing department would be responsible for the price variance while the production department would be responsible for the quantity variance. To compute the direct labor price variance subtract the actual hours of direct labor at standard rate 43200 from the actual cost of direct labor 46800 to get a 3600 unfavorable variance.

There are two reasons for this. 410 hrs Standard Quantity SQ 7x20000 140000 sq. 40 or 40 Unfavorable In this case the actual price per unit of materials is 900 the standard price per unit of materials is 700 and the actual quantity purchased is 20 pounds.

To compute the direct materials price variance subtract the actual cost of direct materials 297000 from the actual quantity of direct materials at standard price 310500. Textbook solution for Accounting 27th Edition WARREN Chapter 23 Problem 3DQ. Actual Quantity 50 times Standard Price 700 and Standard Quantity 025 times Standard Price 700 combine to point to Second row box.

The amount of materials needed to produce one unit of output 2. The direct material quantity is computed as follows. Material variances include two factors.

Decisions made by the purchasing manager may affect the direct materials efficiency variance for the production manager. Actual cost was 25000. Direct Material Price Variance.

Causes for Direct Material Cost Variance. Actual cost was 17000. Direct Materials and Direct Labor Variances At the beginning of June Bezco Toy Company budgeted 19000 toy action figures to be manufactured in June at standard direct materials and direct labor costs as follows.

We have step-by-step solutions for your textbooks written by Bartleby experts. FLike direct material standards direct labor standards also consist of two components. Actual Quantity x Standard Rate.

Direct Materials cost variance For instance if materials costs are higher than expected the direct material cost variance will be unfavorable. Direct material cost variance is caused due to the following reasons. First overhead absorption is a loose guess ie.

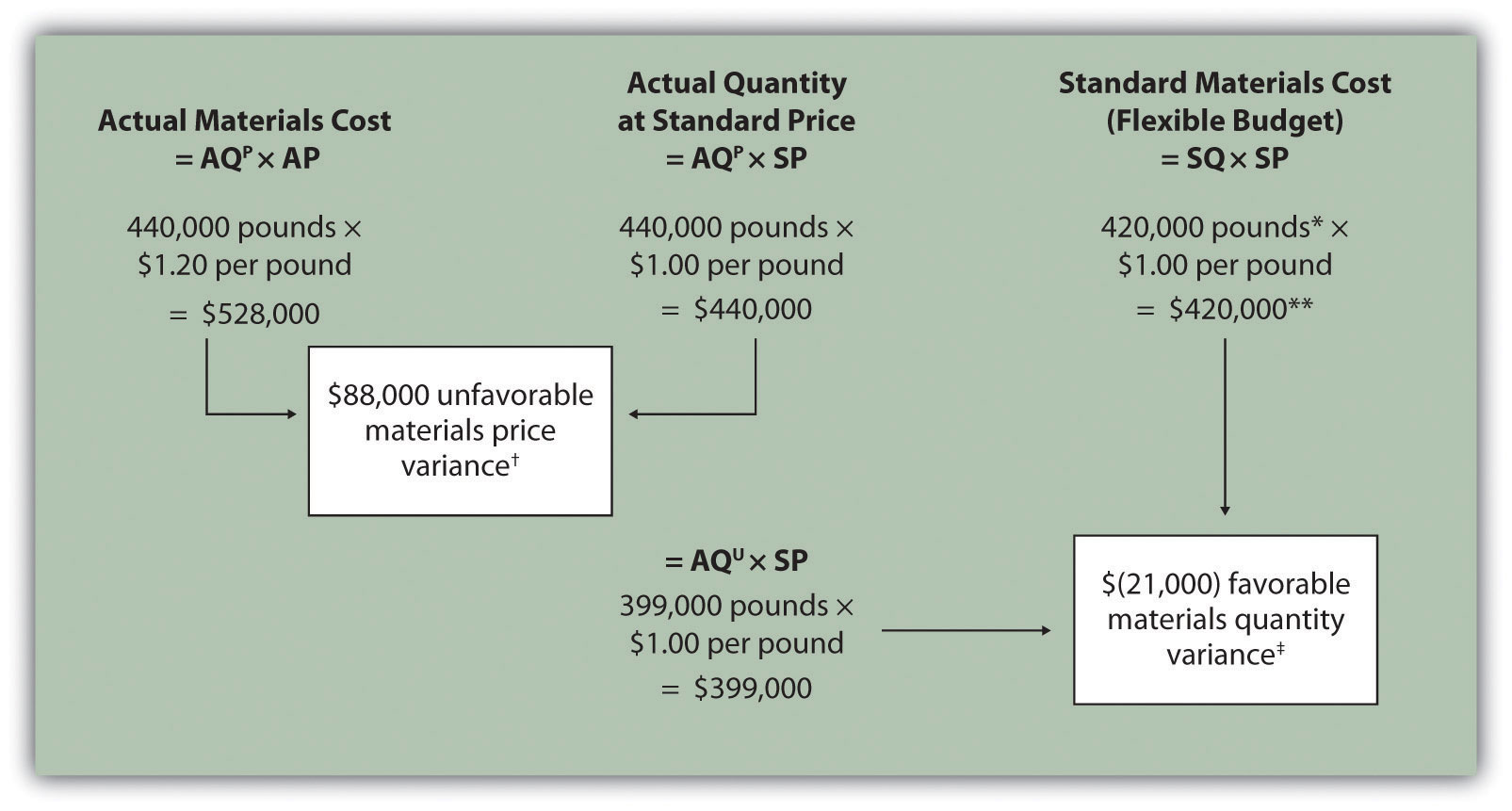

520 Formula Variance Direct. The two direct materials variances are the materials price variance and the materials quantity variance. Materials quantity variance AQ U SQ SP 399 000 42 0000 1 00 21 000 favorable.

Factory overhead volume c. The components of the total direct materials cost variance are the _____ variance and the _____ variance. Favorable variances result when actual costs are less than standard costs and vice versa.

Ft 1200 Actual Quantity AQ 146000 sq. Change in the mix of more than one type of materials in the process of manufacture. 25000 pieces purchased at the cost of 048 per piece.

Note that both approachesthe direct materials quantity variance calculation and the alternative calculationyield the same result. What are the two factors of materials variance. Actual Quantity x Actual Rate.

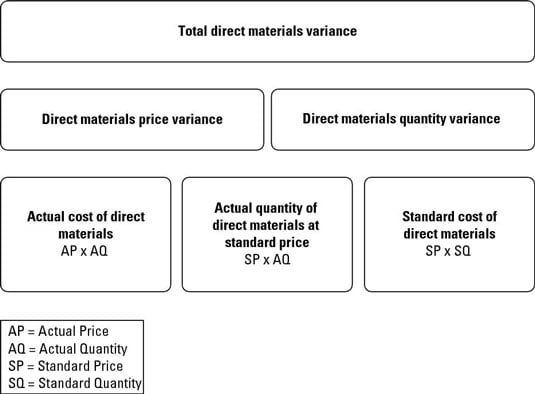

The Direct Material Variance based on actual cost and standard costs are divided into the following two categories. Direct Materials Price Variance 900 700 20 lbs. The direct materials cost variance is also found by combining the direct materials price variance and the direct materials quantity variance.

By showing the total materials variance as the sum of the two components management can better analyze the two variances and enhance decision-making. This is happened due to. What is the formula to calculate material variances.

The prices that should have been paid to acquire this quantity of materials. Adding these two variables together we get an overall variance of 3000. Direct Materials efficiency variance For instance if it is taking more raw materials to assemble a product than expected the direct material efficiency variance will be unfavorable.

A Calculated in Requirement 1 b 17 per DLHr 2140 DLHr 36380 Requirement 3 There may be trade-offs between the direct materials cost variance and the direct materials efficiency variance. The direct materials quantity variance is caused by using too much or too little material. Direct Labor Variances.

Perhaps HearSmart used better quality direct materials.

Direct Materials Price Variance Double Entry Bookkeeping

How To Compute Direct Materials Variances Dummies

Direct Materials Variance Analysis Accounting For Managers

No comments for "The Two Variances in Direct Materials Cost Are"

Post a Comment